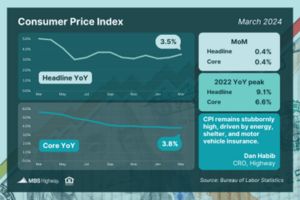

The latest Consumer Price Index (CPI) showed higher-than-expected inflation in March, with the headline reading up 0.4% from February. On an annual basis, CPI moved in the wrong direction, rising from 3.2% to 3.5%. The Core measure, which strips out volatile food and energy prices, increased 0.4% while that annual reading remained at 3.8% (though it was expected to decline to 3.7%).

What’s the bottom line? March’s hotter-than-expected consumer inflation report continues a trend we’ve seen in recent months, as rising energy and shelter costs have added to pricing pressure. Price stability is part of the Fed’s dual mandate. When inflation became rampant a few years ago, the Fed began aggressively hiking their benchmark Fed Funds Rate (the overnight borrowing rate for banks) to slow the economy and rein in inflation. While inflation has fallen considerably after peaking in 2022, the progress lower has slowed, which could delay the Fed’s timing for rate cuts this year. Given that maximum employment is the other part of the Fed’s dual mandate, a cooling job market with rising unemployment could pressure them to cut the Fed Funds Rate sooner rather than later. However, the overall strength of March’s Jobs Report, including the falling unemployment rate, will likely not add any pressure to their timeline.